A Complete Beginner’s Guide

1. The Question Every Indian Investor Asks

“Should I invest monthly or just put everything in at once?”

Every week, someone asks me this at Financial Friend — our financial planning practice in Jaipur. And every time, I tell them the same thing: there’s no single right answer. But there IS a right answer for YOUR situation, and that’s what this guide is all about.

If you’ve ever gotten a bonus and wondered whether to invest it all at once, or if you’ve been setting aside ₹5,000 a month but aren’t sure it’s the smart way — this is for you.

The fear of “what if the market crashes right after I invest?” is real. So is the worry of “what if I miss the rally by waiting?” Let’s break all of this down in plain, simple language — no MBA required.

Reality Check: Most beginners overthink this choice. Both SIP and lump sum can build real wealth — the key is starting, not perfecting.

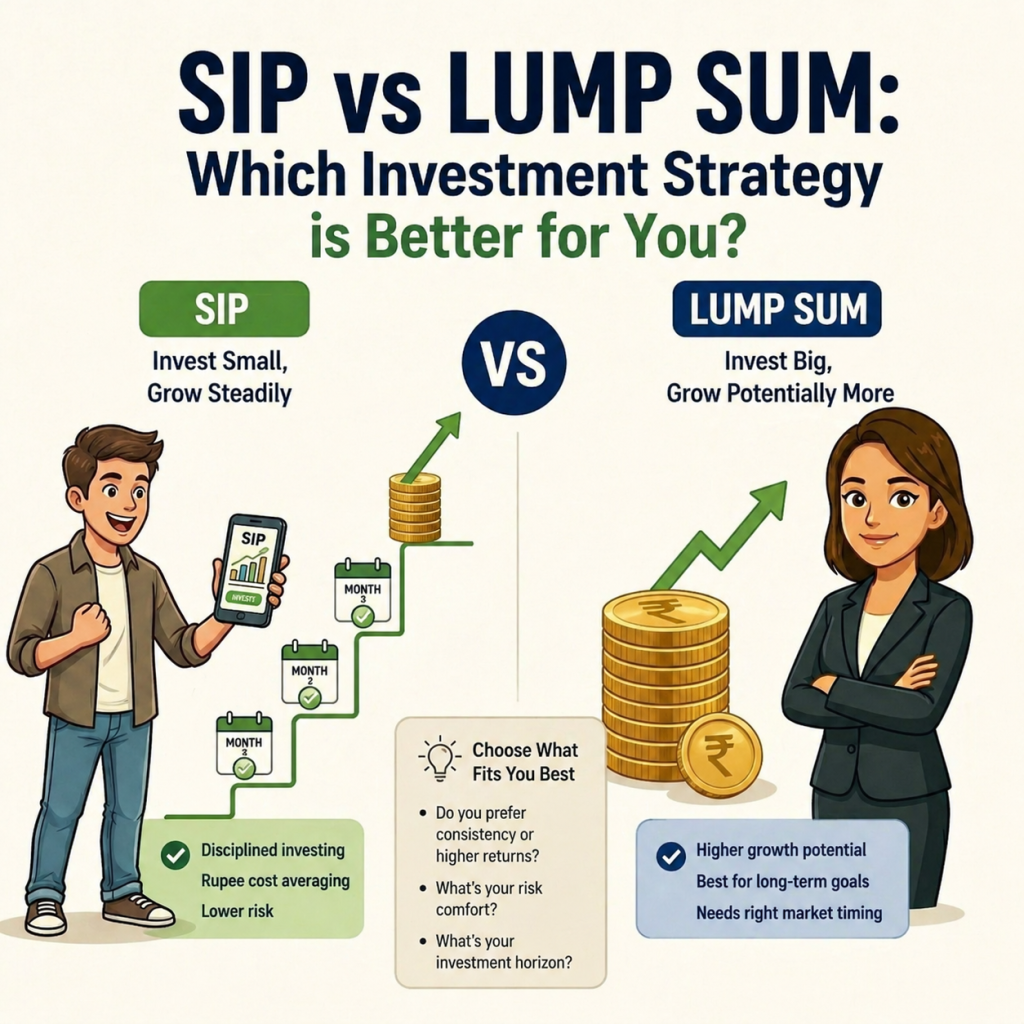

2. What is SIP? (Systematic Investment Plan)

Think of SIP like your grocery subscription. Every month, on a set date, a fixed amount leaves your bank account and gets invested into a mutual fund — automatically.

You don’t need to watch the market. You don’t need to pick a “good time.” The system does it for you.

Simple Example:

Priya, a schoolteacher in Jaipur earning ₹40,000/month, sets up a SIP of ₹5,000 every month into an equity mutual fund. On the 5th of each month, ₹5,000 is automatically invested. Over 10 years, she’s put in ₹6 lakh — and if the fund has grown at around 12% annually, her corpus could be ₹11–12 lakh or more.

That’s the power of consistency. No stress, no timing, just steady building.

• Minimum investment: as low as ₹100–₹500 per month

• Auto-debit from your bank account

• Can be paused, increased, or stopped anytime

• Works for equity, debt, hybrid mutual funds

3. What is Lump Sum Investment?

A lump sum investment means investing a large amount — all at once. Instead of spreading payments over months or years, you put the whole sum to work on a single day.

This is typically done with bonus money, an inheritance, proceeds from a property sale, or accumulated savings sitting idle in a bank account.

Simple Example:

Rajesh, a business owner in Jaipur, receives a ₹2 lakh client payment in January. Instead of letting it sit in his savings account earning 3.5% interest, he invests the full ₹2 lakh into a well-rated equity mutual fund. If markets are at a reasonable level and grow at 12% annually, this ₹2 lakh could become around ₹6.2 lakh in 10 years.

But here’s the catch — if Rajesh had invested right before a market crash, the value might dip initially before recovering. That’s the risk of lump sum.

⚠️ Common Mistake: Many investors invest lump sums when markets are at all-time highs (following FOMO), then panic when values dip. This is exactly what you want to avoid.

4. SIP vs Lump Sum — Quick Comparison

| Feature | SIP | Lump Sum |

| Investment Style | Fixed monthly amount | One-time bulk investment |

| Risk Level | Lower (spread out) | Higher (market timing matters) |

| Market Timing Needed | No | Yes (ideally) |

| Ideal For | Salaried individuals, beginners | Business owners, bonus earners |

| Flexibility | High – start/stop anytime | Low – once deployed |

| Rupee Cost Averaging | Yes (built-in) | No |

| Returns in Bull Market | Moderate (buy at avg prices) | Higher (if timed well) |

| Returns in Bear Market | Better (buy cheap units) | Lower (if poorly timed) |

| Minimum Amount | As low as ₹500/month | Usually ₹1,000–₹5,000+ |

| Emotional Discipline | Easier to maintain | Harder – fear at market dips |

If you’re new to investing and want to understand the basics first, you can start with this complete mutual fund guide for beginners.

5. How SIP Works — The Magic of Rupee Cost Averaging

Here’s the beautiful thing about SIP that most people miss: you WANT the market to fall sometimes.

When prices drop, your fixed ₹5,000 buys MORE units. When prices rise, it buys fewer. Over time, your average cost per unit becomes lower than the average market price. This is called Rupee Cost Averaging — and it’s the secret weapon of SIP investors.

Example — ₹5,000/Month SIP Over 3 Months:

| Month | Amount Invested | NAV (Price/Unit) | Units Purchased |

| January | ₹5,000 | ₹50 | 100 units |

| February | ₹5,000 | ₹40 | 125 units |

| March | ₹5,000 | ₹25 | 200 units |

| Total | ₹15,000 | Avg: ₹38.33 | 425 units |

Even though the market fell (from ₹50 to ₹25), your average cost is ₹38.33 — not ₹50. You’ve automatically bought more when prices were cheap. That’s rupee cost averaging doing its job.

�� Pro Tip: Don’t stop your SIP when markets fall. That’s actually when SIP is working hardest for you, buying more units at lower prices.

6. How Lump Sum Investment Works

With lump sum, everything rides on the entry point. If you invest ₹1 lakh when the market is fairly valued or at a low, your returns can be spectacular. But if you invest at a peak, you may see your investment in the red for months — sometimes years.

[Insert image: market volatility graph showing peaks and corrections]

Example — ₹1 Lakh Lump Sum Scenarios:

• Invested at market bottom (Jan 2020 pre-rally): ₹1 lakh → ~₹2.1 lakh by 2023

• Invested at market peak (Jan 2022): ₹1 lakh → dropped to ~₹82,000 within 6 months

• Long-term view (10 years, any entry point): Usually recovers and grows to ₹3–4 lakh

The key lesson? For lump sum, time IN the market beats timing the market — but the entry point does matter, especially in the short term.

�� Reality Check: Over 10+ year horizons, even “badly timed” lump sums in quality funds have historically recovered and delivered good returns. The long game matters more than the perfect entry.

7. Which is Better in Different Market Conditions?

In a Rising (Bull) Market

Lump sum tends to outperform in a clear bull market. If you invest ₹1 lakh at the start of a rally, you ride the full wave. SIP, by contrast, buys units at progressively higher prices, reducing your average gain.

But — and this is crucial — no one rings a bell at the start of a bull market. Recognizing it early is extremely difficult.

In a Falling (Bear) Market

This is where SIP shines. Every monthly installment buys more units as prices fall. By the time the market recovers, your lower average cost means higher profits.

A lump sum investor in a bear market either has to hold on with nerves of steel or risks panic-selling at a loss.

In a Volatile (Sideways) Market

Volatile markets — like what we’ve seen throughout 2024–2025 — are where SIP’s rupee cost averaging is most powerful. Your SIP quietly accumulates more units during dips.

�� Pro Tip: In volatile or uncertain markets (which describe most of 2026 globally), SIP is generally the safer and smarter default choice for most investors.

8. When Should You Choose SIP?

SIP is ideal for you if:

• You have a regular salary or monthly income

• You are new to investing and don’t understand market cycles

• You want to invest without monitoring markets daily

• You tend to get anxious about market ups and downs

• You have a long-term goal — child’s education, retirement, home purchase

• You want to build the habit of disciplined saving

In my experience working with investors across Jaipur, most salaried professionals benefit enormously from SIP. It removes emotion from the equation and turns investing into a automatic habit — like paying your EMI.

Once you decide to invest through SIP, the next step is choosing the right funds. You can explore our list of best SIP mutual funds in India.

9. When Should You Choose Lump Sum?

Lump sum makes sense when:

• You have received a bonus, incentive, or windfall

• Markets are in a significant correction (valuations look attractive)

• You have idle money sitting in a savings account or FD earning low returns

• You have a very long investment horizon (10+ years)

• You are investing in less volatile funds like debt or balanced funds

• You are an experienced investor comfortable with short-term volatility

⚠️ Common Mistake: Don’t invest your emergency fund as a lump sum. Always keep 3–6 months of expenses liquid before investing. Investing money you might need soon is a recipe for panic-selling.

10. Can You Combine Both? (The Smartest Approach)

Yes — and honestly, this is what I recommend most often.

The hybrid approach: Use SIP for your regular monthly savings AND deploy lump sums whenever you receive extra money. This gives you the best of both worlds.

Here’s How it Works in Practice:

• Set up a monthly SIP of ₹5,000–₹10,000 from your salary

• When you receive annual bonus (say ₹50,000–₹1 lakh), invest a lump sum

• Consider STP (Systematic Transfer Plan) — park lump sum in liquid fund, then auto-transfer to equity fund over 6–12 months

STP is particularly powerful — it reduces the risk of bad market timing while ensuring your money isn’t sitting idle. Think of it as a lump sum that gradually converts to SIP.

�� Pro Tip: STP (Systematic Transfer Plan) is the best-kept secret in mutual fund investing. Park your lump sum in a liquid fund, and automatically transfer ₹10,000–₹20,000 per month into your equity fund. You get safety AND growth.

Whether you choose SIP or lump sum, selecting the right mutual fund is crucial. Here’s a simple step-by-step guide to choosing the right mutual fund.

11. Real-Life Scenario Examples

Scenario 1: Salaried Employee — Kavita (Age 28, Jaipur)

Kavita works in IT and earns ₹60,000/month. She wants to build a ₹50 lakh corpus for retirement.

Best strategy: SIP of ₹8,000/month in a diversified equity fund. At 12% annual returns over 20 years, she’d accumulate approximately ₹79 lakh — exceeding her goal.

Scenario 2: Business Owner — Mahesh (Age 42)

Mahesh has ₹5 lakh in his current account after a good quarter. The money is earning just 3.5% in savings.

Best strategy: Invest ₹5 lakh via STP into an equity fund over 10 months. This gets his money working without full market-timing risk.

Scenario 3: Annual Bonus — Sunita (Age 35)

Sunita receives a ₹1.5 lakh Diwali bonus. She already has a SIP running.

Best strategy: Invest ₹1 lakh as lump sum (market was at a correction in late 2025), and keep ₹50,000 as emergency reserve top-up.

12. Common Mistakes to Avoid

⚠️ Mistake 1: Trying to time the market perfectly — nobody can do this consistently, not even professional fund managers. Time in the market beats timing the market.

⚠️ Mistake 2: Stopping your SIP when markets crash — this is the WORST thing to do. A market crash means your SIP is buying units on sale. Stay invested.

⚠️ Mistake 3: Investing your entire life savings as lump sum at market peaks due to FOMO (Fear of Missing Out). Always check valuations or use STP.

⚠️ Mistake 4: Ignoring your investment for years without review. Review your portfolio at least once a year with a qualified advisor.

⚠️ Mistake 5: Not linking investments to a goal. “I’ll invest and see” leads to panic decisions. Define your goal, timeline, and required amount first.

13. Why You Need a Financial Advisor

Here’s the truth that most finance apps won’t tell you: the biggest enemy of investment returns isn’t a bad fund — it’s your own emotional decision-making.

In March 2020, when markets crashed 40%, millions of investors redeemed their mutual funds in panic. Those who stayed invested (or added more) saw their investments triple by 2021. Those who sold, locked in losses permanently.

A good financial advisor doesn’t just pick funds. They:

• Help you stay calm during market volatility

• Build a strategy aligned with your actual life goals

• Ensure your asset allocation is appropriate for your age and risk appetite

• Prevent costly emotional mistakes

• Review and rebalance your portfolio annually

The value of advice isn’t in stock tips — it’s in preventing the one catastrophic decision that wipes out years of gains.

14. Why Investors in Jaipur Should Seek Expert Guidance

Each investor needs a completely different strategy. A salaried person with ₹5,000/month free cash needs a different SIP plan than a businessman who has ₹5 lakh sitting idle every quarter.

If you’re looking for a mutual fund advisor in Jaipur who understands these local nuances — not just generic fund recommendations — the right guidance can make a significant difference in your long-term outcomes.

The best mutual fund advisor in Jaipur isn’t the one who gives you the highest projected returns on paper — it’s the one who builds a plan you’ll actually stick to.

15. Why Choose Financial Friend, Jaipur

At Financial Friend (www.financialfriend.in), we’ve been helping investors across Jaipur build personalized, goal-based financial plans for years.

What makes us different:

• We start with your goals — retirement, child’s education, home purchase — and build backwards

• We recommend both SIP and lump sum strategies based on your actual income patterns

• We use STP wherever appropriate to reduce market-timing risk on larger amounts

• We’re available year-round for review — not just at account opening

• We simplify jargon and explain every recommendation in plain language

We believe financial planning should feel like talking to a trusted friend — not sitting across from a salesperson. That’s why we’re called Financial Friend.

Ready to start your investment journey? Visit www.financialfriend.in or Call us at 9460825477 for a free consultation.

16. Frequently Asked Questions

Q1. Is SIP safer than lump sum?

In most cases, yes — especially for beginners. SIP spreads your investment over time, reducing the impact of market volatility. Lump sum can be equally safe if you invest during market corrections and have a long horizon.

Q2. Which gives better returns — SIP or lump sum?

In a consistently rising market, lump sum tends to give higher returns because your full capital compounds from day one. In a volatile or falling market, SIP typically wins due to rupee cost averaging. Over very long periods (15–20 years), the difference often narrows.

Q3. Can I switch from SIP to lump sum later?

Absolutely. You can run both simultaneously, stop one, or start the other at any time. Most investors use both strategies across their portfolio.

Q4. What if the market crashes right after my lump sum investment?

Stay calm and stay invested. Historically, every market crash has been followed by recovery. If you’ve invested in a quality diversified fund with a 5–10 year horizon, short-term dips are just noise. The bigger mistake is panic-redeeming.

Q5. Can beginners invest lump sum?

Yes, but with caution. Beginners should ideally start with SIP to build comfort with market movements. If you do invest a lump sum as a beginner, use STP — park the amount in a liquid fund and transfer monthly into equity funds.

Q6. What is the minimum amount for SIP?

Many funds allow SIPs starting at ₹100–₹500 per month. There’s no maximum limit. Even ₹1,000/month in a good equity fund, started early, can build meaningful wealth over 15–20 years.

Q7. Should I stop my SIP during a market crash?

No — this is one of the most common and costly mistakes. A market crash is when your SIP is actually working best, buying more units at lower prices. Stopping during a crash locks in paper losses and breaks the compounding cycle.

Q8. What is STP and when should I use it?

STP (Systematic Transfer Plan) lets you park a lump sum in a low-risk liquid fund and automatically transfer a fixed amount into an equity fund each month. It’s ideal when you have a large amount to invest but want to avoid timing risk.

Q9. Is lump sum good for tax-saving (ELSS) investments?

Yes. If you’re investing in ELSS funds for Section 80C tax benefits and want to exhaust your ₹1.5 lakh limit before March 31, a lump sum in ELSS makes sense. However, SIP in ELSS spread across the year can also work well.

Q10. How do I choose between SIP and lump sum for my specific situation?

The best approach is to speak with a qualified financial advisor who understands your income pattern, goals, risk tolerance, and existing portfolio. Generic advice rarely accounts for your unique situation.

Q11. Can I have multiple SIPs?

Yes, and in fact, most investors should. You might have one SIP for retirement (long-term equity fund), one for a child’s education (medium-term balanced fund), and one for a near-term goal (short-term debt fund). Multiple SIPs aligned to different goals is smart planning.

Q12. How long should I stay invested via SIP?

The longer, the better — that’s the magic of compounding. Even 10 years can create significant wealth, but 15–20 years is where SIP truly transforms financial lives. Don’t think of SIP as a short-term savings tool.

Q13. What happens to my SIP if the fund house shuts down?

Your money is protected. Mutual fund assets are held separately by a custodian and are not part of the fund house’s balance sheet. SEBI regulations ensure investor protection even if a fund house faces issues.

Q14. Should NRIs (Non-Resident Indians) choose SIP or lump sum?

NRIs can invest in Indian mutual funds via SIP or lump sum subject to KYC and FEMA regulations. SIP is generally preferred as it removes the need to monitor Indian markets from abroad. Consult a mutual fund advisor familiar with NRI compliance.

Q15. How does inflation affect SIP vs lump sum?

Inflation is actually an argument FOR investing (rather than keeping money in a savings account). Both SIP and lump sum in equity funds have historically beaten inflation over the long term. SIP’s regular investing ensures you’re always deployed, which is a natural hedge against inflation.

Q16. What is the ideal SIP amount for a salaried person?

A general thumb rule: invest at least 20–30% of your monthly income. So on a ₹50,000 salary, a SIP of ₹10,000–₹15,000 is a healthy target. Start where you can and gradually increase by 5–10% each year (step-up SIP).

17. Conclusion — Your Best Investment Strategy in 2026

Let me leave you with what I tell every investor who walks into our office in Jaipur:

There is no universally “better” strategy between SIP and lump sum. The right choice depends on your income, your goals, your risk appetite, and — most importantly — your ability to stay invested through market ups and downs.

SIP is your best friend if you’re salaried, just starting out, or prone to emotional decision-making. Lump sum is powerful if you have idle money, are investing during corrections, or have a very long horizon. The hybrid approach — running SIPs with occasional lump sums and STPs — is what most serious wealth builders actually do.

The most important thing? Start. Don’t wait for the perfect time, the perfect market level, or the perfect strategy. A good-enough plan executed today will beat a perfect plan that never begins.

If you’re unsure where to start, or if you want a strategy tailored specifically to your situation, we’re here to help.

Connect with Financial Friend — your trusted partner for goal-based investment planning in Jaipur.

Further Reading — Recommended Articles

• Complete Mutual Fund Guide for Indian Investors

• How to Choose the Right Mutual Fund for Your Goals

• Best SIP Mutual Funds in India — Our 2026 Picks

About the Author

Hi, I’m Gunjan Kataria, Founder at Financial Friend in Jaipur.

As a Certified Financial Planner (CFP) and Chartered Trust and Estate Planner (CTEP), I specialize in customized strategies that align with clients’ unique risk profiles and financial goals, enabling them to make informed decisions for wealth growth and management.

I help working professionals, women, parents, retirees, and first-time investors make smart money decisions without the jargon.

With years of experience guiding people through budgeting, saving, investing, and retirement planning, I’ve seen one truth:

— Most people don’t need complicated strategies, they need a clear, personalised plan they can actually follow.

What I do:

1. Help you build wealth while enjoying your present life

2. Create customised money plans based on your goals & lifestyle

3. Break down complex financial concepts into easy, actionable steps

4. Provide guidance that’s trustworthy, friendly, and free from product-pushing

I believe personal finance isn’t just about numbers, it’s about freedom, security, and peace of mind.

Whether you’re:

🔹 Starting your career and want to avoid costly money mistakes

🔹 A professional in IT or other fast-paced industries seeking clarity in your finances

🔹 A High Net Worth Individual (HNI), CEO, or business owner wanting a trusted partner to optimize wealth and secure your legacy

🔹Preparing for retirement and aiming for peace of mind

🔹 Or simply looking to manage your money better

I’m here to be your trusted guide and partner in the journey.

Let’s connect and talk about how you can take control of your finances, grow your wealth, and design a life you truly love.

E-mail: gunjan@financialfriend.in

Connect with Us on Social Media for Latest Finance Updates

Linkedin: https://www.linkedin.com/in/gunjan-kataria-financecoach/

Facebook: https://www.facebook.com/financialfriend.in/

Instagram: https://www.instagram.com/financialfriend.in/

Youtube: https://www.youtube.com/channel/UC9lV6UXOuBdvK7lLNsbQGaA

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully and consult a registered financial advisor before investing.